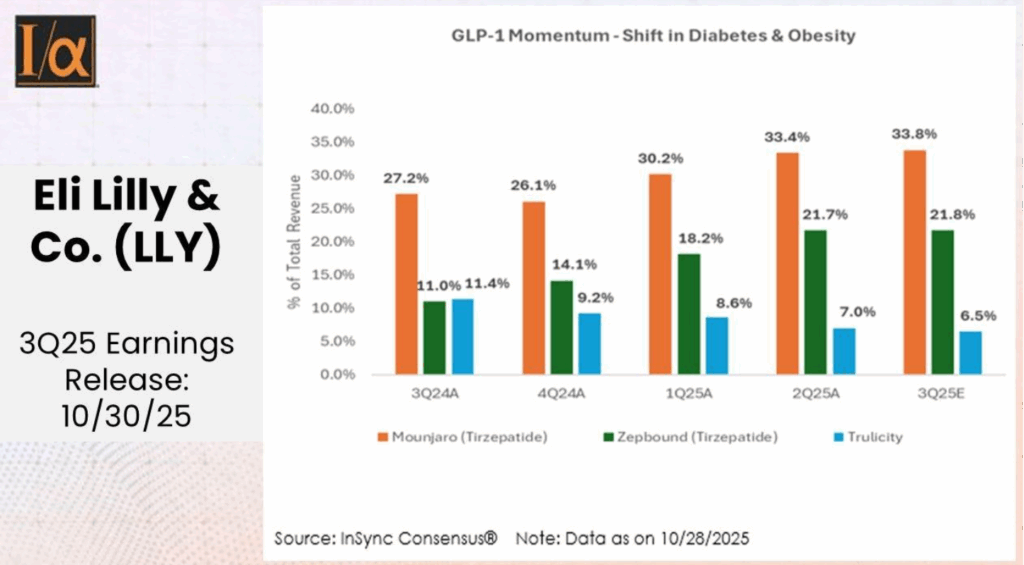

Eli Lilly (LLY) Strategic Shift: Demand for GLP-1 Therapies Rises in Cardiometabolic Care

InSync Consensus® estimate for 3Q25E indicates the following:

Revenue at $16.2B, up 41.4% Y/Y (CER 41.2%), consistent with increased FY25 guidance in 2Q25 ($61.0B vs. $59.5B in 1Q25). GLP-1 drugs—Mounjaro and Zepbound—continue to grow in the cardiometabolic portfolio, reflecting rising global needs in diabetes and weight-loss care.

Stay ahead in earnings with a complimentary trial of InSync Consensus®.

Mounjaro revenue is expected at $5.5B, up 75.8% Y/Y (CER 64.9%). It will contribute 33.8% to the total revenue vs. 27.2% in 3Q24, indicating continued adoption by diabetic patients.

Zepbound revenue is expected at $3.5B, up 180.2% Y/Y (CER 200.0%). Its revenue contribution is forecast to increase to 21.8% from 11.0% in 3Q24, driven by robust demand in weight-loss therapies. However, volume growth may be impacted by CVS Caremark’s exclusion of the drug.

Trulicity revenue is estimated at $1.0B, down 19.7% Y/Y (CER -20.8%), as patients are shifting from Trulicity to Mounjaro.

Oncology

: Verzenio revenue is estimated at $1.5B, up 12.5% Y/Y (CER 9.3%), providing incremental support to the topline amid higher treatment demand and volume growth.

R&D Expenses

: R&D % of revenue continues to be stable at 21%, with increased focus on investments in late-stage pipeline products for Cardiometabolic portfolio. Return on Research Capital (RORC – derived) is expected to increase from 3.91 in 3Q24 to 4.92 in 3Q25E, driven by a consistent increase in Gross Profit (3Q25E Y/Y growth of 43.0%).

EBIT

: EBIT projected at $7.1B (44.3% Margin) vs. $1.7B (15.3% Margin) in 3Q24

EPS

: EPS estimated at $6.42 per share, a 437.8% Y/Y growth (up 1.8% Q/Q), consistent with raised FY25 guidance in 2Q25 ($22.38 vs $21.53 in 1Q25).